Whenever the conversation on property investment comes up among young couples, I always hear the same statements made:

‘Property investment is for the rich people’

‘Investment is risky’

‘When I get a better pay then I will invest’

And I notice this misconception that investing in a Singapore property is a complex activity that only the rich can do.

But, it can start simply by investing in the very home a couple is going to live, and grow their family in.

That is how the 5 Cycles To Amass Cash With My Home framework was created, to show young couples how they can accumlate $1 million in their bank account, beginning from their first home.

Through the 5 Cycles To Amass Cash With My Home framework, families have begun, and managed, to accumulate wealth in their bank accounts by using the home that they own.

From the video above, Ganesh and Pauline is an example of a couple who has managed to build up to $5 million in wealth by their 50s.

But when considering any method to profit from real estate, many families have the same 2 concerns:

1. How do I choose the right property that can make profit?

2. How do I ensure I can afford the monthly installments, even when I lose my job and income?

The good news, is that there is a solution to both these challenges.

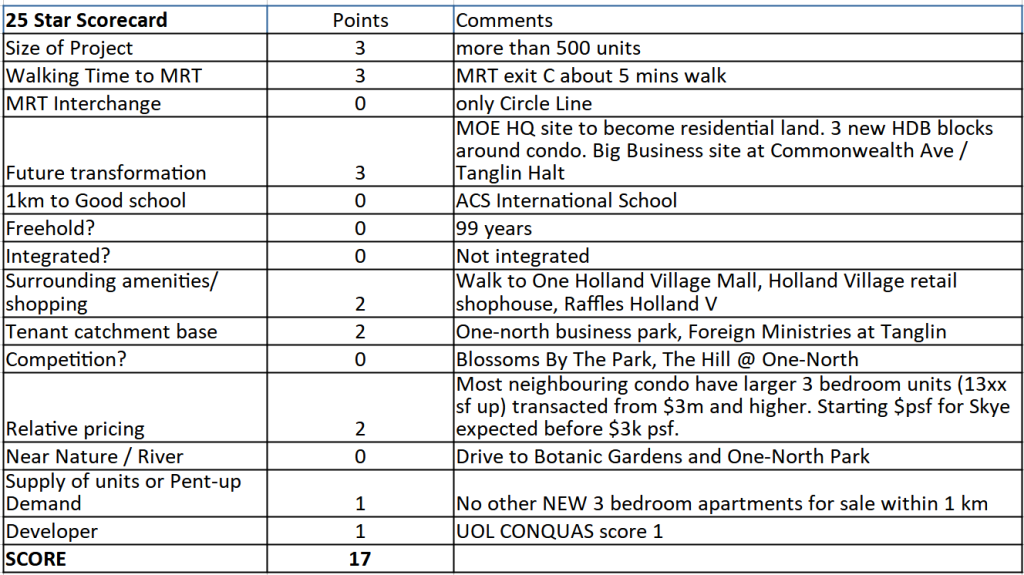

The 25 Star Grading system is a proprietary method where we allocate points to a property to evaluate its investment potential.

It is based on criterias all home buyers look at when choosing a home. Each factor in the method carries a different level of importance, based on how families generally make decisions when choosing the right home.

Here is an example of the 25 Star Scorecard.

This residence scores 17 out of 25 Stars in its grading, which can be compared to another property objectively to determine which is better, using the same method.

In order to manage risks when buying a home, like the risk of losing the home to the bank because the family cannot pay the monthly installments, most families set aside a cash buffer in case of emergencies.

However, how much of a buffer is enough?

If the buffer is too much, then the family may not have enough cash upfront to buy their desired home.

If the buffer is too litte, then the amount may not be enough to cover the time taken to get an income back and repay the loan.

What if interest rates jump? Will the buffer be sufficient to cover the increased monthly installments?

Because of the many possible scenarios, I have come up with a system that overcomes this challenge, by optimizing the cash buffer, so that each family can rest easy throughout the days they stay in their home.

This is called the Home Moving Review.

You can do so with the Amass Cash With My Home Class!

In this FREE class, that will be conducted online, you will learn and be able to implement:

“As a couple looking for our matrimonial home, the framework was very helpful in allowing us to understand each others’ desires and considerations when it comes to property. We both learnt something new about our preferences as well!

With that clarified, it became easier for us to pinpoint what we wanted. In the end, we were able to select a home that fit our requirements and at a reasonable price.”

Chong Tat & Natalie

“We were staying in a condo, but had plans to move to a bigger one and also to get an investment property in the future (moving up to the third cycle). There were many parts of the property buying process that we have yet to look at, so this framework was helpful in piecing all the different parts together to form a clear picture for us.

With a plan in place, it was easy for us to zoom in to what we wanted, and after seeing a few housing options, we chose one that suited our needs quickly and at the best price.”

Troy & Alicia

So you can register your interest in the form below, and we will be contacting you soon to advise on the next available session.